While barriers to private brand adoption in discretionary categories are eroding, other categories remain national-brand dominant.

South Africa’s FMCG landscape is undergoing a structural shift and private brands are no longer a side story. They are now central to how retailers compete, how manufacturers allocate production capacity (and shelf space) and how shoppers make decisions under financial pressure.

According to the latest Trade Intelligence (Ti) Private Brands Report, private brand turnover is estimated to reach R139bn in 2025, accounting for 28.6% of total FMCG sales. This scale firmly positions private brands as a dominant industry force, moving them from the tactical tools they once were, where they competed mainly on price, to core drivers of a retailer’s long-term business strategy, brand identity and profitability.

While retailers are strengthening their differentiation, manufacturers must actively decide how to engage with their retail partners, whether through partnership, competition or a hybrid approach.

The trust advantage

The trust advantage

“The foundation of growth in private brands lies in the more functional, price-sensitive and essential categories like flour, maize meal, rice and sugar,” explains Caroline Short, research and advisory services lead at Trade Intelligence.

“This is because staples are anchors of trust, so if they deliver consistently on quality and price, this builds shopper confidence.”

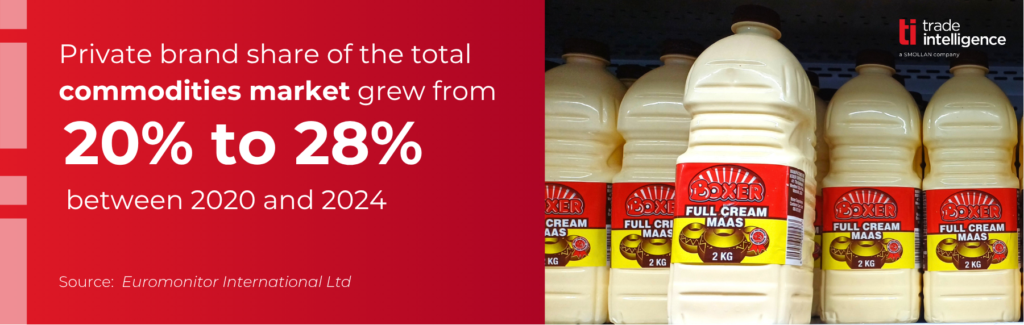

Private brand share of the total commodities market grew from 20% to 28% between 2020 and 2024. And building equity in these categories enables retailers to expand their private brands into more complex or emotionally driven categories.

“For manufacturers, this underscores a massive risk, however,” continues Short, as losing share in staples can have a ripple effect, leading to declines in broader brand equity and, with it, share loss. Long-term, it could also impact manufacturing efficiencies and trigger an overall drop in market relevance.

Taking share in the treat aisle

Taking share in the treat aisle

Private brand penetration within certain discretionary categories is also expanding. In 2024, confectionery private brands grew +24.7% YoY in value, versus total category growth of +10.81%. Even when under financial pressure, shoppers are not necessarily exiting indulgence categories, turning to affordable alternatives as the default choice for ‘little luxuries’. This signals that value perception is now strong enough to compete even where emotional purchase drivers are high.

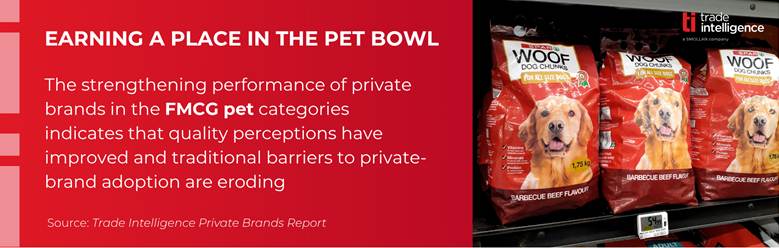

Earning a place in the pet bowl

Earning a place in the pet bowl

The same dynamic is evident in pet care. According to the Ti report, there is strong private brand adoption in this category. This is significant: pet owners want the very best for their four-legged friends, and pet food is typically associated with high trust and perceived risk.

The strengthening performance of private brands in the FMCG pet categories indicates that quality perceptions have improved and that traditional barriers to private brand adoption are eroding.

Not every category is up for grabs

Not every category is up for grabs

Not all categories are equally penetrable, however. Carbonated beverages remain a key exception, with private brands holding just 3% share. According to Ti’s report, entrenched brand loyalty and deeply ingrained taste habits continue to act as barriers in soft drinks.

“Global players like The Coca-Cola Company and PepsiCo have built decades of equity in soft drinks,” explains Short, “so emotional connection and habitual consumption still outweigh price-driven switching in this category.”

Promotions still matter

Promotions still matter

Importantly, price alone is not the defining factor in shopper decision-making when it comes to private brands. In fact, 44% of shoppers trying to save money would rather search harder for promotions before switching to private brands. This presents a clear defensive strategy for national brands. Instead of relying solely on price cuts, brands can protect share through targeted, strategic promotions that reinforce value without eroding long-term positioning.

The stokvel opportunity

The stokvel opportunity

Finally, the report points to a major opportunity within collective buying behaviours. According to Ti’s research, 91% of stokvel members claim they would buy private brands if bulk discounts are agreeable. Retailers that tailor private brands strategies for stokvels through pack sizes, pricing, and targeted offers have the potential to unlock scale in this channel.

Winning the next phase

Winning the next phase

The overarching takeaway from Ti’s research is clear: “Private brands are no longer a binary choice between ‘cheap’ versus ‘premium’,” concludes Short.

“They form part of a sophisticated, multi-tiered strategy that is reshaping shopper behaviour, how retailers differentiate themselves and the decisions manufacturers make.”

The real question for industry players is no longer whether private brands will grow, but how to position themselves to win within their rise.

{kind=link}