The structural decline of news media’s traditional business model – advertising and circulation revenue – has hovered like a dark cloud over publishing strategies for 20-plus years. But the continued focus and momentum of diversifying revenue streams over the last years is helping publishers to reach a more balanced and sustainable business model.

That is just one of the reasons that publishers gave us in our latest World Press Trends Outlook survey for feeling optimistic about the future – despite the myriad challenges the industry is facing.

The findings included in the latest World Press Trends Outlook report are based on insights from over 170 senior media executives across 66 countries, providing a global snapshot of the trends shaping the future of publishing.

“Certainly much of the key metrics and narratives associated with news media today – and included in our report – reflect a shrinking and challenged industry to say the least,” said Dean Roper, director of insights at WAN-IFRA. “Despite that, the survey responses and insights shared by publishers for this edition do not paint a picture of an industry in retreat or retrenchment, but more so one of innovating and adapting in the face of relentless change.”

————————————————————————————————————

The full World Press Trends Outlook 2025-2026 report is available for download exclusively for WAN-IFRA Members in our Knowledge Hub. (If you are not a member and interested in the report or joining WAN-IFRA, please contact us.)

————————————————————————————————————-

Below are some of the report’s highlights.

1. Revenues enter the ‘three-pillar model’ era

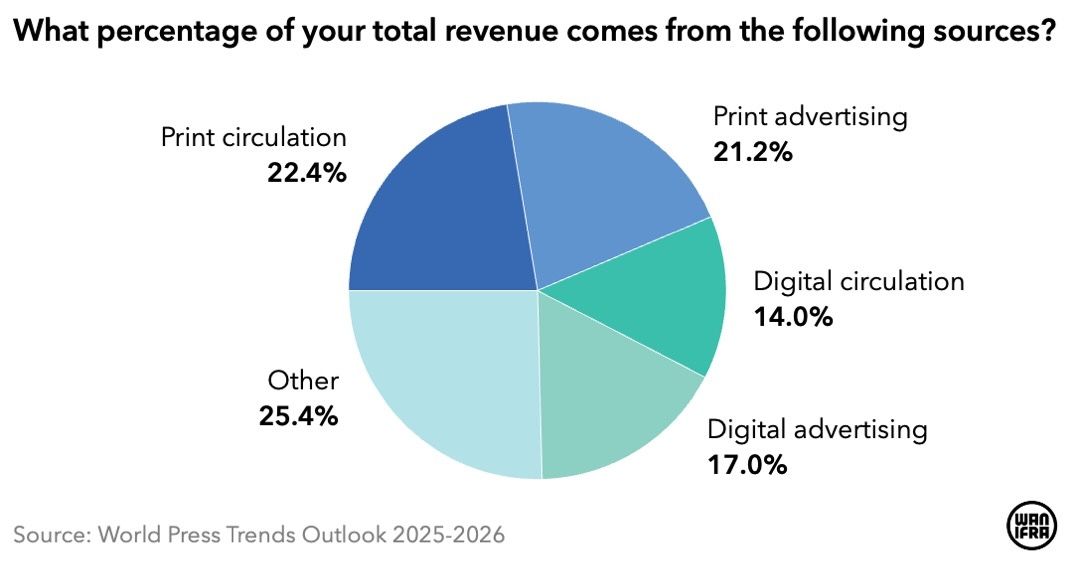

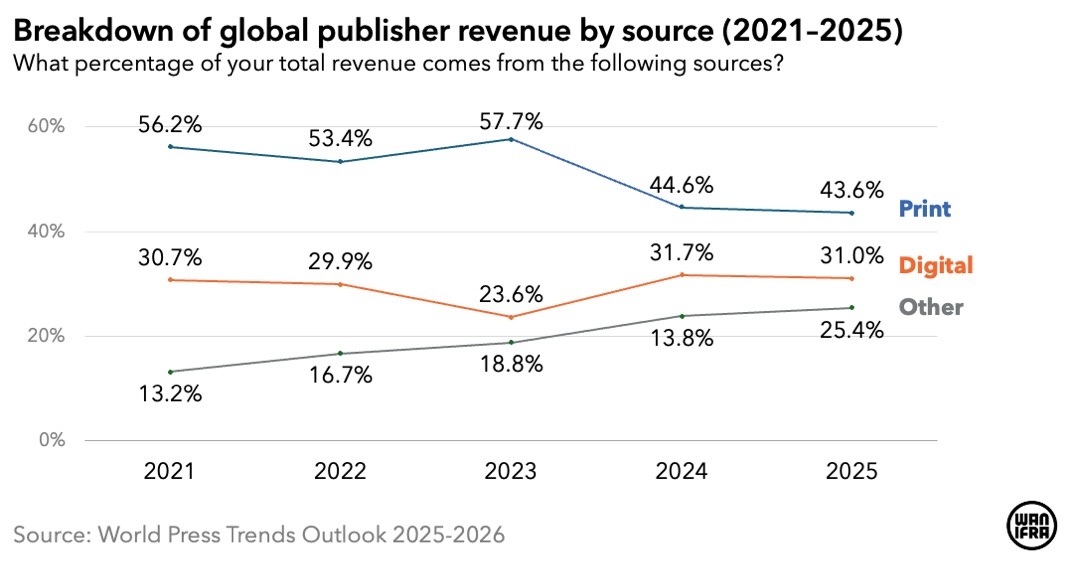

Print remains a resilient revenue source, with print circulation and advertising together accounting for 43.6% of our respondents’ total income and print overall remaining their largest single revenue source.

However, the gap with other income sources is narrowing. Digital circulation and advertising together now represent 31% of respondent’s revenue, while income from other activities (events, B2B services, e-commerce, etc.) now accounts for an average of 25.4%.

When compared with data from our previous annual surveys, the trend is clear: over the last five years, print has declined from representing 56.2% of publishers’ total revenue to 43.6% today – a drop of almost ten percentage points.

While many publishers rely on growing digital revenues, our respondents indicate that these have mostly stagnated at around 30% over the last five years. Within this, digital circulation has largely been on a slight upward trend. However, digital advertising has proven to be an unpredictable revenue source (particularly in 2023, when those revenues dipped significantly).

In fact, it is the other revenue sources that have seen most reliable growth over the last few years, increasing from 13.2% in 2021 to more than a quarter (25.2%) today. Events continue to be the main area of activity in this area, with 32.2% of respondents identifying them as an important revenue source, followed by B2B services content and Partnerships with platforms (both 16.1%),

2. AI maturity: From experimentation to strategic integration

Since ChatGPT was launched to the public more than three years ago, artificial intelligence has evolved from a novelty to a core strategic priority for an increasing number of news publishers.

Nearly 93% of respondents identified AI and Automation as a top investment area for the coming year, closely followed by a related area Data Analytics and Intelligence, which is an investment priority for 90% of respondents.

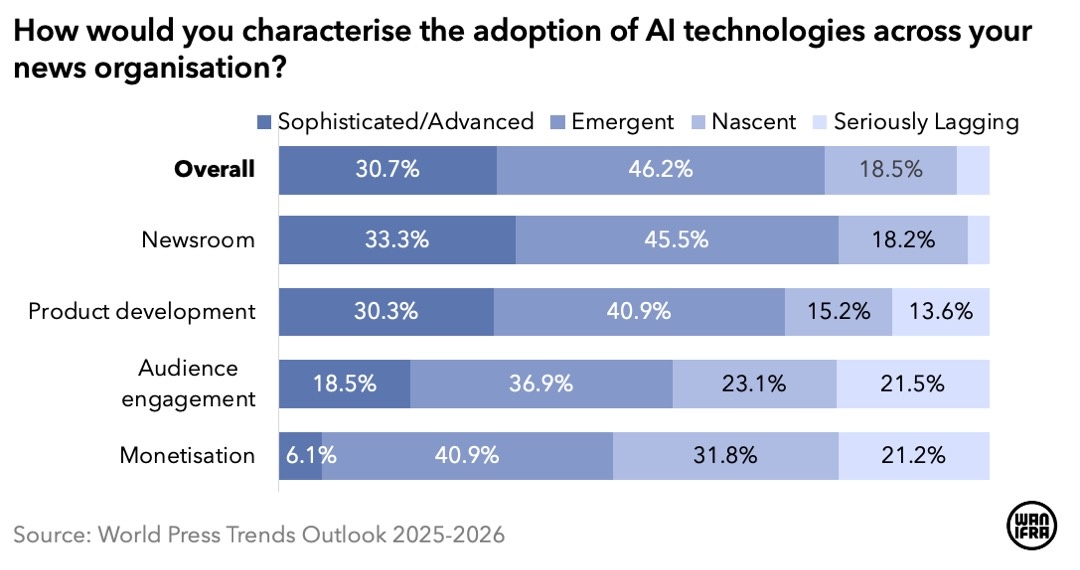

Meanwhile, responses from publishers concerning AI adoption reveal that, although they are seeking to harness AI across their businesses, adoption levels vary between organisational areas.

Overall, 30.7% of respondents say that their AI adoption at a Sophisticated/Advanced level, while 46.2% say it is Nascent. Adoption appears strongest in newsroom operations, while there is still significant room for growth in using AI for monetisation and audience engagement.

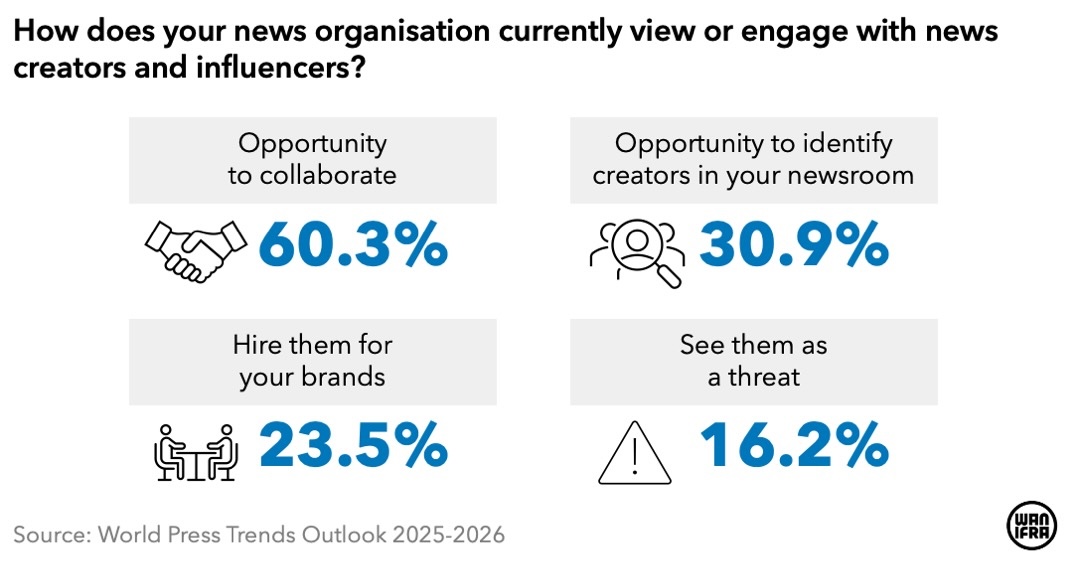

3. Publishers joining hands with influencers

In light of the growing creator economy, news publishers are quickly seeking to position themselves with regard to this fast-growing sector of the media landscape. Attitudes towards creators and influencers vary, but based on our results, the majority of publishers are optimistic about working with creators, with 60.3% viewing them as an opportunity for collaboration.

Moreover, one third of respondents said they see opportunities in producing creator-like content internally within their newsrooms, while almost a quarter said they are hiring creators directly to work with their news brands. Only about one in six see this growing area of the media as a threat.

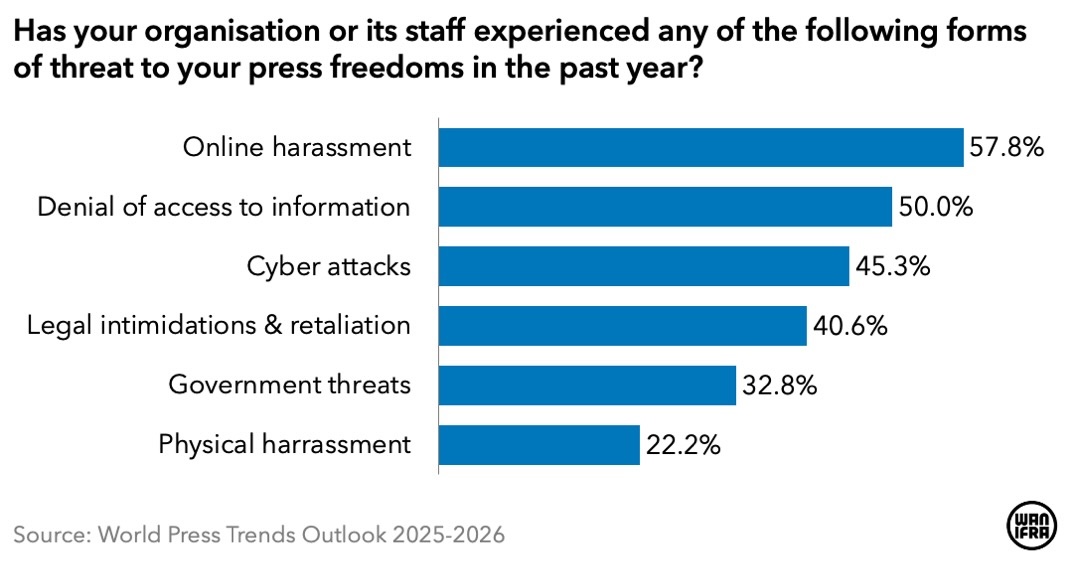

4. Media freedom: A global crisis of erosion

As several international organisations have pointed out, media freedom is under severe pressure in an increasing number of countries, and attacks on media and press freedom continue to be seen around the world. This is also reflected in the experiences of our respondents.

Almost half (45.5%) of those surveyed said that media freedom had worsened in their country over the past year. Just over one in ten (10.6%) reported improvements in this area.

Our data shows that the majority of threats to media freedom are occurring in the digital sphere. Online harassment is the most prevalent threat, reported by 57.8% of the organisations featured in the report, followed by denial of access to information (50.0%). Almost half (45.3%) represented news organisations experienced cyberattacks in 2025.

Teemu Henriksson is research editor at WAN-IFRA.

The full World Press Trends Outlook 2025-2026 report is available for WAN-IFRA members to download for free. World Press Trends is supported by Stibo DX.

{kind=link}