The latest RAMS released in September by the BRC and SAARF indicates that we’re listening to radio one minute less, which seems to be having an impact on overall listenership trends, which are heading south.

There are 296 radio stations reported in South Africa: 40 are commercial/public stations and 256 are community stations. Community radio stations to date have grown by 38 in 2015 alone, but listenership has also dropped.

Radio listenership is down across most of the time channels, and most stations, but notably across the morning and evening drive times. This results in advertisers paying the same, or often more, for lower audience. Marketers however know that these two dayparts have the highest rates, so it would be wise to ask your strategist/planner to compare the CPM values to a year ago, or even period ago. And Saturday and Sunday morning audiences, where value was always massive, also reflect a high loss of audiences in general.

Who is losing audiences and who isn’t?

More radio stations have lost listeners than gained. Smaller stations such as PowerFM and RiseFM have gained the most listeners (off a low base), while HeartFM, Pulpit and KFM have lost considerable numbers. If marketers are looking for value for money, then the top gaining radio stations are possibly a consideration (if the listener market fits). Needless to say, the losers should be re-evaluated by marketers and media planners.

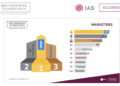

The top radio stations by audience

The top radio stations by audience

Note: Eight of the top 10 radio stations (average day listenership) belong to the SABC. UkhoziFM is unsurpassed with a whopping 7.386m weekly listeners – if we ignore the combined total of the 256 community radio stations.

If the industry still can’t see the wood from the trees in terms of the numbers yet, I would suggest they investigate the quality of the listeners. I bet you will see huge top-end quality (LSMs) among the top 10 radio stations, outweighing smaller stations “presumed to have top quality radio audiences”. Yes, we will have to consider wastage, but wastage is also relative and becomes a negotiating tool at sales level and not necessarily at the selection level. I would rather have more, and new, listeners being exposed at a discounted cost, than smaller numbers at a high cost to the campaign.

Top radio stations with high exclusive listenership are a plus to any campaign, but not a necessity. Retail campaigns will possibly be more inclined to rely on frequency strategies and would therefore require more duplicated listenership between stations. The top radio stations are also language dependent, with the result that they have ‘exclusive’ listenership.

Six of the stations with the highest exclusive listenership are also part of the top 10 favourite radio stations, Ukhozi, Umhlobo Wenene, Lesedi, Thobela, Motsweding and RSG.

The status of community radio stations is healthy, although there was a slump in listenership. It would make business sense to add more radio stations in KwaZulu Natal and Mpumalanga, because of the higher provincial population profiles in these provinces compared to the rest of the country, reflecting fewer community radio stations. (Profiles are recorded by main AMPS)

Generally profiles have not changed for South African radio, since the last few diaries. We have more women than men listening to radio, aged 25+, and with a slight skew towards 50+. Listener profiles are also representative of the SA population’s ethnic groups.

People across the country are listening on average one minute less to radio than the previous diary.

Really, is this significant? Before reading anything into this- such as more time with social media- let us see if it establishes itself as a real trend. The latest RAMS released in September, by the BRC and SAARF, reflects one minute less hours radio listening than a year ago. Interestingly, three provinces have higher listenership than the national average of 3h15, namely North West (3h38), Limpopo (3h57) and top of the list the Free State with 4h07 listening time. Western Cape has recorded the lowest time, namely 2h50! The beach? Wine?

But are marketers voting with their budget? Seemingly not.

Radio grew by 7.7% (R461m) YoY (Aug – Jul). Not shabby at all, if one takes into consideration that radio lost R112m from various categories during the latest recorded period. Radio remains in third place after TV and print in Share of Media with 16%. (While marketers increasingly still look to TV as their main communication medium, with a 3% spend increase, to 52% for the measured period.)

Major growth for radio came from the automotive category with 29% (R178m). Retail also was healthy – it grew by 14% (R165m). FMCG and government were the two categories punishing radio in the latest recorded period with almost half the value spent than previously. But then government spending is always unpredictable, depending on campaign strategies and political events.

Conclusion?

Radio is thriving as a medium. We must remember that DTT is also going to make the playing fields more equal, when all radio footprints will be disappearing resulting in potentially huge shifts of audiences. This could really make the radio medium more appealing to marketers. At the same time, we can expect huge competition amongst the radio stations for survival. There will be casualties. Of course the strong will survive, but one never knows what the underdog can do.

Source: Nielsens RAMS release September 2015; Addynamix August to July.

Sandra Burger is business unit head at The MediaShop. This analysis was first published in the company newsletter, Shop Talk.

{kind=link}